Animals

Animals Animation

Animation Art of Playing Cards

Art of Playing Cards Drugs

Drugs Education

Education Environment

Environment Flying

Flying History

History Humour

Humour Immigration

Immigration Info/Tech

Info/Tech Intellectual/Entertaining

Intellectual/Entertaining Lifestyles

Lifestyles Men

Men Money/Politics/Law

Money/Politics/Law New Jersey

New Jersey Odds and Oddities

Odds and Oddities Older & Under

Older & Under Photography

Photography Prisons

Prisons Relationships

Relationships Science

Science Social/Cultural

Social/Cultural Terrorism

Terrorism Wellington

Wellington Working

Working Zero Return Investment

Zero Return InvestmentTaking Stock

Why Microsoft's Stock Options Scare MeYou can't buy cool with a bunch of Seattle-centric, flannel-shirted mini-Bills driving new Ford Expeditions, wallowing in their overheated stock options and soaring sense of self-worth. World-class creativity requires more than rational thinking. It takes a certain madness. - Jeffrey Young

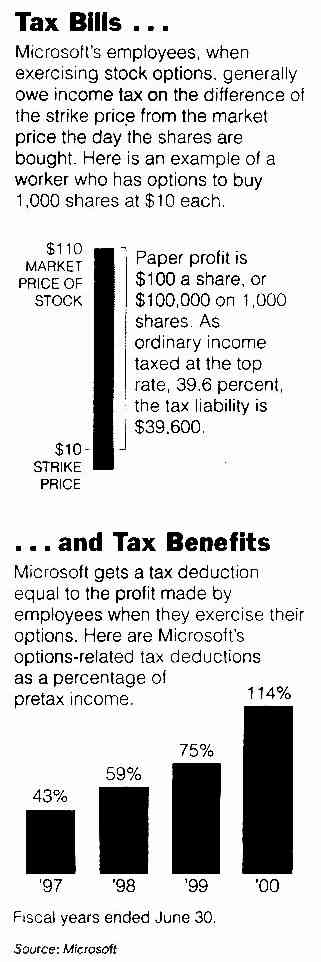

Source: nicholsoncartoons.com.au by Rob Landley Forget Windows 2000. As far as I can tell, the single most lucrative product Microsoft (Nasdaq: MSFT) sells is its own stock. Microsoft receives almost as much cash inflow from the stock market as it does by selling goods and services. Here's how: Basically, Microsoft receives cash by issuing employee stock options, after which the company then receives billions of dollars in tax deductions from the IRS for doing so. Add in the warrants it sells on its own stock, and the company made over $5 billion off the stock market last year (fiscal year ended July 1999), tax-free. For comparison, its after-tax net income was only $7.8 billion. Microsoft may not be much in the programming department, but its accountants are impressive. Let's run through that again a little more slowly, using Microsoft's most recent annual report (see www.microsoft.com/msft/ar99/cash.htm). As with all annual reports, the most interesting stuff is in the tables at the end. In this case, search for the $3.1 billion dollar item "Stock option income tax benefits," which occurs in the Financing section of the Cash Flows Statement (the above link will take you there). Lemme detour for a sec to explain what "Stock option income tax benefits" are. A significant portion of the wages Microsoft pays to its employees comes in the form of stock options rather than in cash. Compared to the rest of the industry, the amount of cash Microsoft pays its programmers is at best mediocre. It attracts and retains employees via stock options. These options give the employees the right to buy a certain number of shares of Microsoft stock at a tiny fraction of the current market price. Employees can even take an automatic payroll deduction to make the token payment to exercise each stock option as it matures, and thus effectively get shares of Microsoft stock as part of their wages (because the stock has appreciated substantially since it was granted at an exercise price equal to the market price several years prior). Microsoft's options are "non-qualified," which means the employee is immediately taxed when an option is exercised (i.e., used to actually purchase very cheap stock). The difference between the price the employee pays for the stock and the current market price for the stock they receive is counted as taxable income on the employee's W-2 tax form for the year, as if they'd received it in cash. The cost basis for the stock is adjusted accordingly, meaning that if the employee immediately sold their newly acquired Microsoft shares they wouldn't incur any additional taxes. They've already been taxed on that income anyway, and the only new taxes to accrue are capital gains taxes if they sell the stock for a higher price than they bought it at. (Capital gains taxes apply to the extra money gained by selling an investment for more than it was purchased for. Only the amount over the original purchase price - the cost basis - is taxed, and this has nothing to do with options.) Corporations pay taxes on their own income (generally 35%), but money they pay out in salaries to employees is deductible from the corporation's income. Since granting options to employees results in taxable income to those employees, Microsoft gets to deduct that taxable employee income from its own taxable corporate income, and that's where Microsoft got a tax-free $3.1 billion in cash in fiscal 1999: "Stock option income tax benefits." But if you stop and think about it, Microsoft didn't really have to spend actual money to provide the options. It even GOT a little money from its employees, in the form of the cash the employees paid (via payroll deductions) to exercise their options. All Microsoft had to do was issue new stock certificates, which more or less involves taking a vote in a board meeting and then firing up a laser printer. So Microsoft got $3.1 billion of tax money back from the government, which at a 35% tax rate would be in exchange for a $9 billion tax expense it never had to pay. Its employees got taxed and paid that tax out of their own cash wages, and Microsoft got the money refunded back into its corporate coffers. It even got $1.3 billion of cash BACK from its employees in that payroll deduction to exercise the options (the "Common stock issued" line item, in the same Financing table as the "Stock option income tax benefits"). Together, that's almost $4.5 billion dollars Microsoft made directly from selling stock. This is on top of a huge cash savings from substituting shares of its stock for actual cash paid to employees in the first place. Remember, Microsoft only made a $7.8 billion net profit last year. To pay its employees an extra $9 billion in cash compensation expense, it would go $1.2 billion into the red. But it doesn't have to, as the stock market provides the money to keep Microsoft going. Microsoft prints stock, pays its employees with the stock, and the stock market provides the cash for Microsoft's employees when they sell the stock or get margin loans against it. Microsoft can print as much stock as it likes in order to pay its employees, and as long as the market keeps wanting to buy shares from those employees, then Microsoft doesn't have to spend too much of its own cash to pay its people. As of July '99, Microsoft had around $60 billion of employee stock options outstanding, and it grants more all the time. Of course printing more stock dilutes the value of Microsoft's existing shares, but as long as the stock price keeps going up nobody seems to mind. And of course Microsoft can buy back some of its shares - $3 billion in 1999 ("Common stock repurchased" in the same Financing table as before) - but since it issued over $10 billion worth of shares ($9 billion taxable income over and above the $1.3 billion the employees paid for it), this buyback is a mitigating factor at best. But since a lot of Microsoft shareholders hold on to their shares and live on margin loans, the dilution doesn't increase Microsoft's share float until they do decide to sell (that is, the stock starts going down and they have to pay off those margin loans). Meanwhile, the buybacks help keep the stock price from dipping too much. Employee options aren't the only kind Microsoft sells. It sells another kind called "put warrants" to mutual fund managers, giving them the right to sell Microsoft shares back to the company at a fixed price (well below the price they're currently trading at, of course). Mutual fund managers with a large exposure to Microsoft stock buy warrants as insurance, giving them a guaranteed floor price they can sell out at if the stock collapses. If the stock doesn't collapse, the warrants expire worthless after a few years, and provide Microsoft with additional revenue (three quarters of a billion in 1999, "Put warrant proceeds" in the cash flows statement). So there you have it. $3.1 billion from a tax loophole, $1.3 billion from its employees, and $0.7 billion from put warrants combine to give Microsoft over $5 billion from its own stock in fiscal 1999. And it avoided paying $9 billion in wages. All that from a company that only had $7.8 billion in net income. And as long as the stock keeps going up, they can keep doing that ad infinitum. Maybe if Microsoft had recruited a few people from their accounting department into the programming staff, they'd have gotten Windows 2000 out on time, eh? Then again, who cares about products if you can make this much money without them? - Oak Source: www.fool.com 17 February 2000 Also see:

Some Suffer Tax Hangovers from Microsoft Option SpreeDuring the 1990's, Seattle echoed with tales of Microsoft millionaires, ordinary workers who became wealthy from stock options the company had awarded. Now that Microsoft's stock has fallen to about half its peak, Seattle is abuzz with other stories, those of Microsoft employees deep in debt and filing for bankruptcy. Mike Fitzgerald, the trustee overseeing Chapter 13 bankruptcy filings by individuals in the western district of Washington, estimated recently that he had seen 25 cases filed by Microsoft workers related to options. "These stock options looked so good that people lost track of what they were intended to do," he said. "They were a second-tier excuse for Microsoft instead of paying them a real salary. It's really a world of hurt." As at other technology companies, the woes of workers at Microsoft stem in large part from tax bills incurred when the options were exercised. Worse still, some people who were experienced engineers and programmers yet naIve about the stock market turned their options into stock and then borrowed against those shares to pay their taxes. The high-risk practice, known as a margin loan, is more often a tool of speculators aiming to buy additional stock without additional money. As the stock fell, these workers' shares were sold, leaving them broke. One midlevel Microsoft employee said that a broker at Salomon Smith Barney, the firm hired by Microsoft to administer its option program, pushed him to take such risks. At the peak, his shares were worth about $1.5 million. But last fall, when the stock began to dive, the firm began selling shares out of his account to payoff the loan. Now most of his stock is gone and he owes $100,000 in taxes, more than he makes in a year and more than he has. His only remaining asset is a modest Seattle home, which he and his wife fear they will lose.

Lena Diethelm, an enrolled agent at the tax preparation firm Number-shuffler in Palo Alto, California, said she had heard many similar stories from workers in Silicon Valley and faults brokers for urging employees to borrow to pay taxes. "I think these practices are predatory," Ms Diethelm said. "The brokerage firms have conflicts of interest, but the employees don't understand the relationship the companies have with each other. They don't understand the risks, and the brokers minimise the risks." When a brokerage firm oversees a corporate option program, it has two masters: the company that pays it and the company's employees, who are often steered its way for financial advice. The brokerage firm is paid to help employees exercise their options, and it profits when employees bring it additional business. Likewise, the company that issues options reaps tax breaks and can get other financial benefits when employees exercise them. Microsoft and Salomon Smith Barney, which is now part of Citigroup, maintain that there was no conflict of interest because their contract extended only to the exercise of options and employees were free to approach any firm for financial advice. Any advice comes from a division of Salomon separate from the one it pays for administration, Microsoft noted. Susan Thompson, a Salomon spokeswoman, said, "They're actually entirely separate businesses that serve different clients and different client needs." But it is no surprise that many Microsoft workers wind up taking financial advice from Salomon. In company documents, Salomon is identified as Microsoft's "preferred broker" and employees are told they can "take advantage of additional products and services" by opening a full-service account at Salomon. When asked whether Salomon has a policy governing its customers' use of margin, the firm declined to comment. But its Web site says "margin accounts can be very risky, and they are not suitable for all investors." Among the risks described, "you can lose more money than you have invested" and "you may be forced to sell some or all of your securities when there is a decline in your account equity value." Microsoft recognised early on that options allowed it to attract talented employees and keep salaries in check. The company and its workers benefited as the stock surged. The Microsoft worker who told his story on the condition that he not be identified said he had not planned to turn the options into stock for some time, believing Microsoft's price would continue to rise. Because the difference of the price of the option from the market price of the stock on the day of purchase, known as the spread, would be taxable as ordinary income, the couple would have a big tax bill. Most people sell shares immediately to pay the taxes, as the couple had done in the past. The couple was persuaded to buy some 20,000 shares with options in 1999 and 2000 by Salomon Smith Barney, they said, and advised to put the shares in a margin account to generate cash for taxes and other expenses like home improvements. Larry Feinstein, a partner at the law firm of Bortman & Feinstein in Seattle, has a handful of Microsoft employees as clients who borrowed against their shares to pay taxes. "These are middle-management people that all of a sudden have to file bankruptcy," he said. "The brokers are more than happy to loan you the money and charge interest on it." Having borrowed against the shares, the programmer and his wife received calls for cash from their broker when the stock fell last year. Although rules at brokerage firms vary, a customer who pledges stock for a margin loan may have to put up more money when the shares decline to 40% of the value of the loan. When the couple could not put up more cash, their shares were sold to meet repeated margin calls. They now have a looming tax bill and virtually no equity. Salomon, they said, did not fully explain the risks of margin. "They should have been a lot more forthcoming with the information," the programmer said. "We did not get into the stock market voluntarily. We were paid in stock and were forced into the stock market with stock options. We trusted our broker to have our best interests at heart." Lewis D Lowenfels, an authority in securities law at Tolins & Lowenfels, a law firm in New York, said that the broker in this case might have run afoul of the suitability requirements of the National Association of Securities Dealers. "It does not appear to be suitable to take people with these limited means and to leverage them so that their entire net worth is at the mercy of fluctuations in the price of Microsoft stock," he said. Salomon's profits on the margin loan taken by the Microsoft programmer were sizable. According to a computation by the worker's accountant, the annual interest charged by Salomon on his margin loan was $60,000 to $80,000 - roughly his yearly salary. At one point the loan, which fluctuated based both on the level of borrowing and the stock price, approached $800,000. Of course, there are times when it is wise to cash in stock options. Most employee options have a finite life. People who are convinced the stock is going higher may choose to exercise options before they expire, pay the taxes on the income that is generated and hold the shares so that any future profits are taxed at the lower long-term capital gains rates. According to the couple in Seattle, the Salomon broker made this argument in late 1998. Roughly 40% of the programmer's options would begin expiring in three years, the broker said, so they should start turning them into shares. Initially, the couple rejected the idea because of the tax bill it would create. Then came a different pitch. "The stockbroker said one reason to exercise the options was because if I got hit by a bus, my wife would have no access to them," the programmer said. Only recently, when the couple reread the option plan did they find that the options would have gone to her if he had died. The Salomon spokeswoman said: "We don't comment on anonymous allegations." The Microsoft programmer now acknowledges that it was a mistake to rely on his broker to the degree that he did and not to read the documents before deciding to exercise the options. Like Salomon, Microsoft stood to benefit when its employees exercised their options. The company gets a tax deduction equal to the spread on which the employee pays income taxes. In fact, the tax break has greatly reduced and in some cases eliminated tax bills at profitable corporations like Microsoft, Cisco Systems and Dell Computer in recent years. And when workers exercise options, they help their employer in another way, by reducing the number of options outstanding. Around the time the programmer and his wife say they were encouraged to exercise options, Microsoft was under pressure from institutional investors to reduce its options outstanding. By 1999, the number of options that Microsoft had set aside for grants had ballooned. Pat McGurn, president of Institutional Shareholder Services, said that the amount of Microsoft options, which dilute the voting power and value of existing shareholders, was roughly three times the recommended level in its industry. "The real problem is that these plans are growing so quickly," Mr McGum said. "So companies have made a conscious effort in recent years to get people to push more options through the pipeline." Caroline Boren, a Microsoft spokeswoman, said the company had never tried to influence personal financial decisions of its employees. "Microsoft cares deeply about its employees and wants them to be successful financially, even in a tough economic climate," Ms Boren said. "The company makes it easy for employees to access and complete transactions regarding their stock options, but ultimately the decisions on how and when to utilise these benefits reside with the employee." While employees receiving options typically have to sign a document to signify their acceptance of the plan's terms, as the programmer did, there is little regulation of such materials to ensure that the risks are clear. This contrasts with employee pension plans, which must disclose benefits and risks in plain English to employees, according to Christine Jolls, professor of law at the Harvard Law School. "Options are a whole new form of employee benefit that has grown up relatively recently," Ms Jolls said. "It does seem to be a new development in the employee relationship that the law hasn't focused on." Mr McGurn said that the prospect of employees being forced into bankruptcy is an unforeseen consequence of the option boom. "We've given options to fairly financially unsophisticated individuals and to people who don't understand the risk inherent in them," he said. "You wouldn't allow these folks to invest in a hedge fund, but we allow them to make six-figure bets on stock options without the benefit of any independent financial advice." Source: New York Times Wednesday 18 April 2001

This topic is continued on the page following this one because I ran short of room on this page. There, you'll find Called to Account ("Stock options must be expensed starting in 2005...") and Destructive Creation ("Many high-tech companies have lent money to their buyers to purchase their products. Now some of those borrowers are finding it difficult to pay them back.")

For more articles relating to Money, Politics and Law including globalisation, tax avoidance, consumerism, credit cards, spending, contracts, trust, stocks, fraud, eugenics and

more click the "Up" button below to take you to the Table of Contents for this section. |

His

tale and those of others who say they unknowingly took on risks raise questions about whether brokers have failed

to live up to regulatory requirements, including the need to determine if an investment or strategy is suitable

for a client. The brokerage firms profited from the interest on margin accounts, while investors suffered.

His

tale and those of others who say they unknowingly took on risks raise questions about whether brokers have failed

to live up to regulatory requirements, including the need to determine if an investment or strategy is suitable

for a client. The brokerage firms profited from the interest on margin accounts, while investors suffered.