Animals

Animals Animation

Animation Art of Playing Cards

Art of Playing Cards Drugs

Drugs Education

Education Environment

Environment Flying

Flying History

History Humour

Humour Immigration

Immigration Info/Tech

Info/Tech Intellectual/Entertaining

Intellectual/Entertaining Lifestyles

Lifestyles Men

Men Money/Politics/Law

Money/Politics/Law New Jersey

New Jersey Odds and Oddities

Odds and Oddities Older & Under

Older & Under Photography

Photography Prisons

Prisons Relationships

Relationships Science

Science Social/Cultural

Social/Cultural Terrorism

Terrorism Wellington

Wellington Working

Working Zero Return Investment

Zero Return InvestmentDrain, Drain, Go Away

Spending AroundIn a world where the time it takes to travel (supersonic) or to bake a potato (microwave) or to process a million calculations (microchip) - Andrew Tobias by Vince Passaro Now we are $63,000 in debt, I think.

The consumer credit-card debt comes to more than $28,000 overall, the interest rolling on like Woody Guthrie's Columbia River. A few times, while our standing as debtors still allowed it, we turned some of that debt over with consolidating loans and by getting newer, lower-interest cards and moving our balances. We may have saved a few hundred dollars, but basically these moves gave us an opportunity to build up more debt, so that we cost ourselves more money in the long run. The cards offered at lower interest rates convert to usury-rate cards in 3 to 12 months. Right now we're averaging 20% annual interest, so the interest alone, compounding and compounding, like a fracture, is around $475 per month. At our tax rate, we have to earn $85,000 a year just to service our credit-card debt, never mind pay it back. - from Who' Il Stop the Drain? Reflections on !he Art of Going Broke Source: Anderson Valley Advertiser Boonville, CA

Credit Facts

Source: The Sunday Star Ledger Morris County, New Jersey 5 August 2001

Source: Funny Times December 2001 funnytimes.com

Plastic Debts Mountby Deborah Sheldon Shoppers spent £9,000 a SECOND on credit and debit cards last year. A massive £285 billion went on plastic, adding up to almost half of the total consumer spending in 2001. But the price is high and one in 12 people owe at least £2,500, say market analysts Mintel. By the end of 2001 plastic accounted for 44% of the £645 billion we spent. In 1992 it was just 15% of the annual £390 billion spent. Bank card use has risen dramatically to £200 million and is now worth more than twice as much as credit card spending. And despite being launched three years later than credit cards, 56% of adults own debit cards against 49% with credit cards. The number of cheques written has dropped by a third in 10 years. Increased credit card payments have led to greater debts and overspending - 4% of holders owe more than £5,000 and 15% owe at least £1,500. Only 37% have no debts or pay off their balance every month. Mintel says that if people owing more than £5,000 paid the minimum 3% off their balance each month it would take nearly four years to clear the debt. Report author Toby Clark said: "This indicates the dangers of letting credit card spending spiral out of control." Source: mirror.co.uk Saturday 10 August 2002

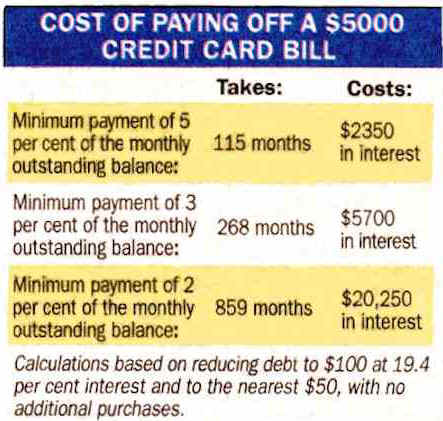

Mintel's estimation of how long it would take to "clear the debt" is interesting.

If all charge card users ceased making any further charges today, I think Mintel would find that it would take most people MUCH longer than 4 years to clear all their credit card debt:

Source: The Dominion Tuesday 6 March 2001

Use Your SmartsA few tips for the smart use of credit cards:

Source: The Sunday Star Ledger Morris County, New Jersey 5 August 2001

Clamp On Credit Cards In NSWby staff reporter Frank Perry The New South Wales Government is to clamp down on access to credit cards after it was revealed the average Australian owes nearly AU$5,500 on credit cards, the ABC reported. The State Minister for Fair Trading, John Watkins, said the Government wanted to stop ban banks from sending unsolicited credit cards to people. "I'm very disturbed at the irresponsible offers of credit card companies that is causing hardship and misery for New South Wales consumers," he said. Mr Watkins said that a state-wide phone-in survey would be launched today asking people to discuss their problems with using credit. Source: newsroom.co.nz 20 November 2000 © NewsRoom See also:

Consumer Debt More Than Doubles in Decadeby Eileen Alt Powell New York - As the bills from holiday spending sprees arrive, Americans are finding that the mountain of debt they've built has gotten even higher. Consumer debt has more than doubled in the past 10 years to record levels, making it hard for many families to cope. For Bruce and Lorraine Esbensen of Clifton Heights, Pennsylvania, trouble started when they spent lavishly on their wedding 6 years ago. They soon found themselves falling behind on their bills. "Creditors were calling, and I knew if I paid one, I couldn't pay the other," Lorraine Esbensen remembers. "It was so painful I got to the point where I didn't want to answer the phone." Credit counsellors helped the couple work out a repayment plan, but it still took more than 4 years to pay down their debt. "We still basically live paycheque to paycheque," she said. "But we do have an IRA (Individual Retirement Account) going now, and we're careful with our spending so we feel better." US Consumer debt hit a record $1.98 trillion in October 2003, according to the most recent figures from the Federal Reserve. That debt - which includes credit cards and car loans, but not mortgages - translates to some $18,700 per US household. At the same time, the government says the nation's savings rate dropped to just 2% of after-tax income in the first half of the year. That means many people lack the means to deal with financial emergencies, much less their eventual retirement. Experts worry about the impact not only on individual families but on society as a whole. "The Depression generation is passing on, and we're losing their values," said Howard Dvorkin, president of the nonprofit Consolidated Credit Counselling Services in Fort Lauderdale, Florida. "Now we've got an entire generation that doesn't know anything about thrift and careful spending. It's tearing the fabric that made this country great." Just how did American consumers get so deeply in debt? Robert D Manning, a sociology professor at the Rochester Institute of Technology who wrote Credit Card Nation - The Consequences of America's Addiction to Credit, says the problem dates back to the 1980s, when financial institutions began issuing credit cards and making loans to people who wouldn't have qualified in the past. "At the same time, people had this sense of entitlement based on the idea that this generation was expected to outperform the earlier generation," Manning said. "It was okay to buy yourself a better standard of living than your parents, and the banks would help you do it." The nation's credit card debt currently stands at $735 billion, or nearly $7,000 per household. And since about 40% of card users pay their balances in full each month, the household card debt of those who carry balances is closer to $12,000. Americans have become champion shoppers, says Joel Greenberg, chief executive officer of the nonprofit Novadebt credit counselling service in Freehold, New Jersey. "Through the go-go '90s, the irrational exuberance wasn't just in the stock markets," Greenberg said. "It was throughout society. We became phenomenal consumers - and deplorable savers." Shopping is what Kristeen Mahler, a secretary from East Meadow, New York, turned to for solace after the 11 September 2001 terror attacks. Mahler's office was just 100 yards from the World Trade Centre. "I shopped to try to forget it," she said. She bought clothes for herself, gifts for friends - and kept the mounting bills a secret even from her husband. Mahler said she finally started talking about the attack and found support from family and friends in dealing with her anxiety. She also sought credit counselling and is one year into a 4-year plan to pay off her debts. What's surprising about the nation's debt is that it has continued to rise despite record numbers of mortgage refinancing from 2001 to 2003, many of them yielding cash that consumers have used to pay down credit card balances. Mark Zandi, chief economist at Economy.com, points out that the rate of growth of card debt has slowed "because people are using their homes as cash machines." But while refinancings have allowed upper income households to put their balance sheets in order, lower income families without that option are finding it harder to cope, he said. "They're the folks filing for bankruptcy in record numbers, they're the ones facing repossession and foreclosures." Consumer bankruptcies have exceeded 1 million a year since 1996, hitting a record of 1.54 million in 2002. Bankruptcy filings totalled 1.25 million during the first nine months of 2003 and could set a new record when full-year tabulations are done by the Washington-based American Bankruptcy Institute. There's debate about how the high debt levels and demanding repayment schedules will affect the economy. Americans currently spend a near-record 18.1% of their after-tax income to cover debts, including mortgages. That limits their ability to borrow more to spend more, and consumer spending accounts for about two-thirds of the economy. Federal Reserve Chairman Alan Greenspan has pointed out that because of low interest rates, consumers can more easily handle their debt so the level is "not a significant cause for concern." Economist Sung Won Sohn of Wells Fargo & Company agrees that for now, most Americans are okay and should continue to be the driving force in the nation's economic growth. Still, he said, the level of debt does raise concerns. "In the long run, it's a ticking time bomb. At some point when you get a sharp setback in the economy or a spike in interest rates, the high debt causes instability." Eileen Alt Powell is a business writer for the Associated Press Source: story.news.yahoo.com Tuesday 6 January 2004

For more articles relating to Money, Politics and Law including globalisation, tax avoidance, consumerism, credit cards, spending, contracts, trust, stocks, fraud, eugenics and

more click the "Up" button below to take you to the Table of Contents for this section. |