The Object of Universal Devotion

Let us not bankrupt our todays by paying interest on the regrets of yesterday and by borrowing in advance the troubles of tomorrow.

- Ralph W Sockman

What's been powering the US economy?

Conventional explanations based on the wondrous flexibility of their labour market don't convince, since those features haven't changed profoundly from the time when their major

economic rivals were outgrowing them. Technological miracles don't persuade either, since there's little difference between productivity growth in the US and in the famously

stagnant EU. Plus, there's strong evidence that almost all reported improvement in US productivity figures in recent years can be traced to the computer industry

alone. Outside computers, economist Robert Gordon estimates that productivity performance in the late '90s is worse than the '72 - '95 average.

To anyone schooled in Keynesian economics, the expansion has been particularly puzzling because it's happened despite substantial fiscal tightening — the budget deficit (almost 5%

of GDP in 1992) was transformed into a surplus of 1% in 1999, a massive shift that might have been expected to render an economy torpid.

So what's been driving it? The growth in debt, says Wynne Godley, of Bard College's Levy Institute. To Godley, the US economy is characterised by seven

unsustainable processes. These are:

- The fall of private savings deep into negative territory.

- A rise in the flow of lending to the private sector.

- Rapid growth in the money supply (the trace of all that borrowing entering the spending stream).

- A rise in asset prices - mainly stocks - at a rate far in excess of growth in GDP or profits. This

contributes to confidence but provides no fresh cash — unlike incomes earned in production, money taken out by selling stock can only be replaced by fresh buying.

- The rise in the federal budget surplus.

- The rise in the current account deficit (the deficit on trade and investment income the US is running with the outside world, which adds to our foreign debt).

- The rise in US foreign debt (when domestic savings fall, and domestic borrowings rise, the shortfall can only be made up from abroad).

In other words, while the US government has grown prudent, the private sector hasn't: both households and businesses are spending more than their income (the income of businesses

being profits).

Source: levy.org

$1.3 Trillion in Deficits Forecast Over Decade

Cumulative Total 60% More than Estimates of Just 4 Months Ago

by Joel Havemann

The budget deficit is becoming a knottier problem in the short term and will be a potentially catastrophic one in the future, the Congressional Budget Office

reported today. The report suggests that President Bush, in the budget he will deliver to Congress in two weeks, will have a harder time keeping his

promise to cut the deficit in half during his presidency. The CBO's annual report on the budget outlook foresees a deficit of $400 billion this year. It

also forecast a cumulative deficit of $1.3 trillion from 2005 to 2014, an increase of nearly 60% from the CBO's $861-billion estimate of just 4 months

ago. These figures take into account some of the administration's request today for another $80 billion for the war in Iraq, but they do not assume an

extension. Nor do they assume the likely extension by Congress of some major tax cuts that were enacted in 2001 and 2003 and are scheduled to expire in 2009 and 2011.

The deterioration in the nonpartisan budget office's budget projection comes despite a somewhat rosier economic outlook than the CBO used in September. Economic

assumptions actually shaved $41 billion from the deficit estimates over the next 10 years. The largest single cause of the rising deficit

estimates was last year's tax bill, which extended marriage penalty relief, the increase in the child tax credit, and the taxation of some income at 10% instead

of 15%. Another factor was a bill providing disaster relief for hurricane victims.

The near-term deficits pale beside the CBO's admittedly rough projections for 2030, when all the baby boom generation will have reached eligibility for Social

Security and Medicare. If they keep growing at current rates, those two programs plus Medicaid for the poor will be nearly as large a share of the

national economy as the entire budget is now, the CBO said. CBO Director Douglas Holtz-Eakin told reporters that the programs would have to be reined in

before that happened. Otherwise, he said, taxes would have to rise to intolerable levels or the government would have to borrow so much money that

interest payments would spiral out of control. "You can't borrow it forever," Holtz-Eakin said. "I don't think you can say deficits don't

matter. They matter a lot."

Joel Havemann is a Times staff writer

Source: latimes.com 25 January 2005

The Last Waltz?: The Coming End of the American Superpower

by Paul Craig Roberts

The US economy is headed toward crisis, and the political leadership of the country - if it can be called leadership - is preoccupied with nonexistent

weapons of mass destruction in the Middle East. The US economy is failing. The afflictions are serious. They could be fatal even if diagnosed and

treated. America is losing the purchasing power of its currency and its ability to create middle class jobs.

The dollar's sharp decline and projections of continuing trade and budgetary red ink are undermining the dollar's role as reserve currency. A number of

central banks have announced that they will be diversifying their currency holdings and will not be buying dollars at the same rate as in the past. This

will put more pressure on the dollar. At some point the flight will begin. Instead of buying fewer dollars, central banks will sell dollars

hoping to get out before the dollar hits bottom. Suddenly, the advantage of being the reserve currency becomes a nightmare as the world's accumulations

of dollars are brought to market. An enormous supply and weak demand mean a very low exchange rate for the once almighty US dollar. Overnight those

cheap goods in Wal-Mart, which are the no-think economist's facile justification for Wal-Mart's decimation of communities, small businesses and employment, shoot up in price.

Interest rates will escalate as the government struggles to finance its endless red ink. Heavily indebted Americans with adjustable rate mortgages

will attempt to sell homes just as rising mortgage rates reduce buyers. Real estate assets, the rising value of which have been keeping the economy going, will give back gains.

The US has lost its ability to create middle class jobs or for that matter any jobs. During the last 4 years the US has experienced a net loss of

760,000 private sector jobs (January 2001 - January 2005). Think what this means for graduating classes and people coming of age to enter the work force. Moreover,

the composition of jobs has changed away from high-value-added, high-productivity jobs in tradable goods and services toward lower productivity

domestic service jobs that cannot be outsourced. Even here in this last remaining area of employment for Americans, the US work force is losing job

opportunities to foreign nurses and school teachers brought in on H-1b work visas as a result of budgetary pressures on local school budgets and hospitals.

No-think economists and politicians continue to propose unemployment insurance and education as remedies for the jobs problem. These proposals are mindless to say the

least. The same incentive to outsource holds for all tradable skills. If truth be known, job outsourcing and offshore production sound the death bell for US higher

education. Americans unable to find jobs in export and import-competitive sectors find themselves searching for jobs in nontradable domestic services, where their inflow into

those labour markets is augmented by illegal immigrants and foreigners on H-1b visas. Obviously,

the pressure on wages is downward.

No-think economists explain away the difficulties as a "globalisation adjustment" that will require Americans to curtail their consumption of imported

goods. These economists are ignorant of American's dependence on imported manufactured goods. Even American brand name goods are made abroad in

whole or in part. Tightening the belt will mean much more than cutting out foreign made luxuries. The dollars' decline will drive up the price of all

inputs except US labour which is being substituted out of production functions and replaced with foreign labour.

Oblivious to reality, the Bush administration has proposed a Social Security privatisation that will cost $4.5 trillion in borrowing over the next 10 years alone! America has

no domestic savings to absorb this debt, and foreigners will not lend such enormous sums to a country with a collapsing currency - especially a country mired in a Middle East war

running up hundreds of billions of dollars in war debt. A venal and self-important Washington establishment combined with a globalised corporate mentality have brought an end to

America's rising living standards. America's days as a superpower are rapidly coming to an end. Isolated by the nationalistic unilateralism of the neoconservatives who

control the Bush administration, the US can expect no sympathy or help from former allies and rising new powers.

Paul Craig Roberts was Assistant Secretary of the Treasury in the Reagan administration. He was associate editor of the Wall Street Journal editorial page and

Contributing Editor of National Review. He is coauthor ofThe Tyranny of

Good Intentions. He can be reached at: pcroberts@postmark.net

Source: counterpunch.org 1 March 2005

He Disagrees

-------- Original Message --------

Subject: Re: Don't read this unless you want to. I don't want to waste your time - not sure if you'd see this that way or not.

Date: Tue, 8 Mar 2005

00:51:14 -0500

From: Cody Hatch <cody.hatch@gmail.com>

Reply-To: cody@chaos.net.nz

To: Ruth Hatch <ruth@chaos.net.nz>

On Mon, 07 Mar 2005 23:31:48 -0500, Ruth Hatch <ruth@chaos.net.nz> wrote:

Suddenly, the advantage of being the reserve currency becomes a nightmare as the world's accumulations of dollars are brought to market. An

enormous supply and weak demand mean a very low exchange rate for the once almighty US dollar.

He says that like its a bad thing. A cheap exchange rate is just what you'd want if you were aiming at export-led growth.

Overnight those cheap goods in Wal-Mart, which are the no-think economist's facile justification for Wal-Mart's decimation of communities, small businesses and employment, shoot up

in price.

That is a bad thing. Of course, he seems to think Wal-Mart is bad, so I'd think he'd think this was good. I'm confused.

The US has lost its ability to create middle class jobs or for that matter any jobs. During the last 4 years the US has experienced a net loss of

760,000 private sector jobs (January 2001 - January 2005). Think what this means for graduating classes and people coming of age to enter the work force.

He starts talking about jobs - then quotes statistics for "private sector jobs". Since we live in a libertarian paradise, the government employs

nobody, so this is fine. Except, er, it isn't, and public sector payrolls have been growing strongly - so much so that it counteracts the net loss in

private sector payrolls - total payrolls have in fact grown. Further, payroll is only ONE way of measuring jobs - and is usually considered the least

accurate. More accurate surveys of employment show much larger gains. Finally, he compares employment figures from the height of a boom to midway into

a recovery. A good economist would at least try to make an apples-to-apples comparison - from one part of the business cycle to the same

part of the next cycle. However, there is a point buried deeply in there. US job growth has been poor (even if positive). But! If exchange

rates fall, we'll see more exports, and fewer imports. This is a recipe for job growth. In fact, a standard talking point of the loony

protectionist fringe is that the flood of cheap goods from China is *causing* the weak job growth. If so, then the current high exchange rate is the

cause, and a low exchange rate is a solution. An economy is a complex interconnected system. Things like exchange rates, interest rates,

employment rates, and balances of trade are not independent variables which rise and fall, but multiple views of the same fundamental process.

Moreover, the composition of jobs has changed away from high-value-added, high-productivity jobs in tradable goods and services toward lower

productivity domestic service jobs that cannot be outsourced.

He misuses the term outsourced - what he actually means is offshoring. More substantively, the jobs being offshored are low-level, low-paid, "grunt"

jobs - call centres, low-level programmers, et cetera. In the IT world, firms are not just hiring, but wages are climbing. In the last year,

software engineer wages rose 8.8%, systems analyst wages rose 6.8%, network and data comms analyst wages rose 7.7%. Given that the consumer price index

rose by only 3.3%, this represents significant gains, and is a sign of scarcity of the most valuable and productive workers.

Americans unable to find jobs in export and import-competitive sectors find themselves searching for jobs in...

Dude! Maybe this is 'cause, like, American exports are really expensive? And like, maybe this would change if they got cheaper? Wonder what could cause that?!

The dollars' decline will drive up the price of all inputs except US labour which is being substituted out of production functions and replaced with foreign labour.

US labour is an increasingly valuable resource. The US imports more physical goods than it exports, but despite the ludicrous fears of those worried

about the offshoring of low-paid call centre jobs, it is a net exporter of services. Further, this surplus is growing.

Oblivious to reality, the Bush administration has proposed a Social Security privatisation that will cost $4.5 trillion in borrowing over the next

10 years alone! America has no domestic savings to absorb this debt, and foreigners will not lend such enormous sums to a country with a collapsing

currency - especially a country mired in a Middle East war running up hundreds of billions of dollars in war debt.

If they won't lend, then it won't happen. If they will lend, perhaps they know something Mr Roberts does not. The rising interest rates he

fears will boost the savings rate, thereby mitigating his point about a lack of domestic savings - which in large part is caused by low interest rates.

A bursting house price bubble and rising interest rates would reduce domestic consumption, increase the savings rate, and decrease the quantity of imports - all

of which would be good things which would help counterbalance the less pleasant effects of these dynamics.

--

Cody Hatch cody@chaos.net.nz chaos.net.nz

"A society that puts equality...ahead of freedom will end up with neither equality nor freedom." - Milton Friedman

Drowning in Debt

Policy Notes 2000/6

by Wynne Godley

The US expansion has been driven to an unusual extent by falling personal saving and rising borrowing by the private sector. If this process goes into reverse,

as has happened under comparable circumstances in other countries, there will be a severe recession unless there is a big relaxation in fiscal policy.

The United States is widely believed to have acquired a New Economy, having achieved the longest economic expansion in its history and the lowest unemployment

rate in 30 years. Untold wealth has been created, productivity growth has accelerated, and inflation has been dormant.

It is generally agreed that the growth of the US economy must soon slow down - or be slowed down by Chairman Alan Greenspan - because unemployment cannot fall much

further without awakening inflation. The question of the moment is whether growth will slow to a rate that just accords with the rate of productive capacity, in

which case there could be a "soft landing." Most people seem to think that if this happens, the good times can continue forever. I, however, doubt that the

expansion can continue at all during the next few years unless there are major changes in the stance and structure of policy.

How Private Spending Has Been Able to Increase So Fast

Although the US expansion has been unusually long, it has not been unusually fast. Growth since 1991 has averaged 3.7% per annum, only 0.2% faster than the

average during the whole postwar period. There have been many 9-year periods during which growth was much faster. It is the growth of private expenditure,

taking consumption and investment together, that has been unusually high, averaging 4.6% per annum.

How could private expenditure have risen so much faster than total output, seeing that it accounts, by itself, for 85% of all the expenditure that makes up the

GDP? How was a quart extracted from a pint pot? In an arithmetical sense the answer is simple. Private expenditure grew faster than total domestic

output mainly because there was a large deterioration in the balance of payments. The pint pot was supplemented by imports of goods and services, which

rose at an average rate of 10.4% per annum. Imports have risen, that is, nearly two-and-a-half-fold since 1991.

However, the deterioration in the balance of payments and a big improvement in the budget were both factors tending to drive private disposable income

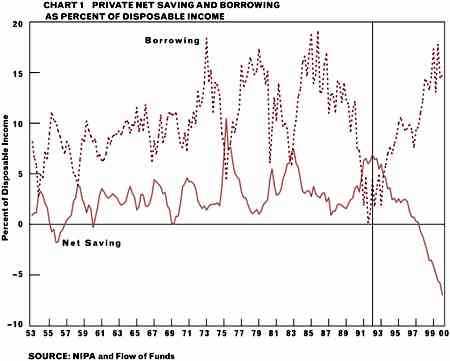

downward. So, again, how was the private sector able to increase its spending so fast? An answer is suggested in Chart 1, in which the solid line shows net

private saving - the gap between private disposable income and private expenditure. For a great many years income consistently exceeded expenditure,

as one would expect; net saving fluctuated quite narrowly, averaging nearly 3% of income. Since 1992 expenditure has risen continuously relative to

income. Net saving fell through the zero line in 1997 and has been falling more and more deeply into negative territory ever since. In the first quarter of

this year net saving reached -7.0% of income and was 9 to 10% below what used to be normal. Whatever this private deficit may portend for the future, it is

certainly entirely different from anything that has ever happened before - at least in the United States.

The general view seems to be that private expenditure has risen because capital gains are being spent; so everything should be all right as long as the stock market

holds up. But it is impossible literally to "spend" capital gains. Either liquid balances must be run down or securities must be realised (that is, sold to

another sector since selling within a sector only shifts money from one pocket to another) - or additional funds must be borrowed.

Figures published by the Federal Reserve reveal that it was borrowing that was the main source of the funds needed to finance excess spending. Borrowing makes it

possible to enjoy capital gains without selling shares and thereby incurring a liability for capital gains tax; also, the interest payable on loans is often tax

deductible. The private sector as a whole has not been realising equities on a substantial scale. Households have been selling equities, but these have been

largely mopped up by corporate purchases. And corporations could only buy equities and simultaneously pay for investment in capital equipment by borrowing more

themselves. According to the Fed's figures, the net flow of credit (advances less repayments) to the nonfinancial private sector taken as whole rose from a

negligible quantity in 1991 to over $1 trillion in 1999, by which time (as the dotted line in Chart 1 shows) borrowing was augmenting disposable income by about 15%.

As the flow of lending to the private sector has been so large, the level of debt has risen in a spectacular way, reaching a record 165% of disposable income in the

first quarter of 2000. Household debt (even if "margin debt" used to finance speculation on the stock exchange is excluded) reached nearly 100% of personal

disposable income - an all-time high. And corporate debt reached 74% of corporate GDP - another record, slightly above the previous peak at the turn of

1989 - 1990, just before the last credit crunch.

Why Private Debt Cannot Increase Indefinitely

It seems fair to conclude, at a minimum, that the high level of debt now poses a risk; if there were a big fall in asset prices or a significant further rise in

interest rates, weak positions might be exposed, which could generate a downward spiral of forced selling. More important, as I shall argue, the combination of

the private deficit and the administration's fiscal plans makes it highly doubtful that the future can be anything at all like the past. The danger of severe and

prolonged recession is being seriously underestimated.

In its April report, the Congressional Budget Office (CBO) published projections of the federal budget through the next 10 years, all based on the assumption that

growth is maintained at about 2.7% per annum, a rate slightly below that of productive capacity, implying that unemployment rises to just over 5%. All

these official projections show the budget surplus continuing to rise throughout the next decade, and recent reports suggest that the rise in the surplus may be

substantially larger than what was projected in the April report.

At the same time the balance of payments deficit looks set to worsen if the economy continues to expand while the dollar remains strong. There has for many

years been a trend deterioration in the US balance of trade, which has been exacerbated, perhaps temporarily, by slow growth in the rest of the

world. However, even if the balance of trade were now to stabilise as the rest of the world recovers, the foreign debt the United States is now incurring is likely

to generate a growing outflow of interest income large enough to make the balance of payments as a whole go on deteriorating.

If the balance of payments does continue to deteriorate, a rise in the budget surplus can occur, as a matter of accounting logic, only if private expenditure

continues to rise relative to income (see Box).

|

Total private income from production of goods and services plus net property income from

abroad (Y) is equal, by definition, to private expenditure (PX) plus government expenditure (G) plus the

current balance of payments (BP). Deduct taxes and transfers (T) from both sides and rearrange to

yield the identity [Y - T - PX] = [G - T] + BP. This formula states that private net saving, the

expression on the left-hand side, is logically equivalent to the government deficit plus the balance of payments surplus.

|

It is impossible to overemphasise that the entire fiscal plan the authorities have set forth, since it combines a rising budget surplus with continued economic growth,

can form part of a coherent macroeconomic strategy only on the assumption that private net saving continues to fall into increasingly negative territory. If

saving does not continue to fall - if private expenditure rises less than income in the years to come - this must (by the laws of accounting) be accompanied by some

combination of a deteriorating budget (that is, a move away from surplus) and an improving balance of payments. And this could happen (given fiscal stance and

trade propensities) only if demand and output in total were to stagnate or collapse. Without a continued stimulus from private expenditure in excess of

income growth, there would be nothing to keep the expansion going. It is theoretically possible, if hardly credible, that a fall in the dollar could result in

a rise in net exports large enough to keep the US expansion going, as happened in Britain after 1992 - after two years of recession.

Yes, but why shouldn't private net saving go on falling, thereby validating the official scenario? Why shouldn't the future, for an indefinite period, be a

"calmed down" continuation of the past? While the United States has never before (at least not in modern times) had a large private financial deficit, there

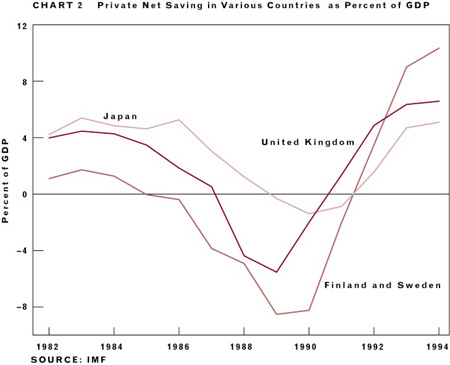

have occasionally been such deficits in other countries. The IMF's most recent World Economic Outlook points to three instances of private deficits - in Japan, the

United Kingdom, and Finland and Sweden (Chart 2). In each of these cases, having reached a negative position not very different from that in which the United

States now finds itself, the deficit recovered over a period of years and regained its habitual state of surplus. In each case, the rise in net saving overshot,

so that for a time the private surplus was unusually high. The period during which the private deficit was growing was always accompanied by an economic boom - acclaimed,

at least in the United Kingdom, as an economic miracle! But each boom was followed by a severe recession as the credit expansion unravelled.

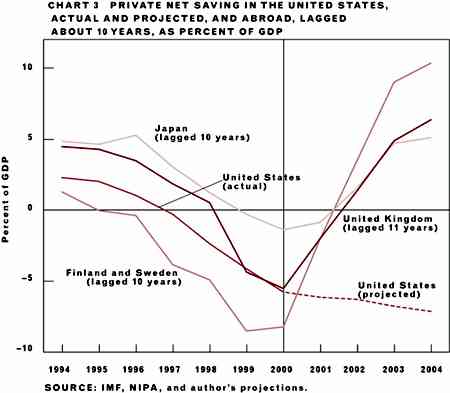

In Chart 3 the path of the United States's private deficit is superimposed on the deficit paths shown in Chart 2. The solid line shows the actual path of the US

private deficit up to the first quarter of 2000; the dash line shows what must be held to happen in the future to validate the CBO's projections. It seems

doubtful, to put it mildly, that things can actually turn out this way. As I argued above, the private deficit can go on rising only as long as net lending

remains at least at its present level, so that private debt continues to rise rapidly relative to income. I reckon that to validate the story illustrated in the

chart, private debt would have to rise to 230% of disposable income in five years' time and continue to rise further thereafter.

An increase in private debt relative to income can go on for a long time, but it cannot go on forever. It is true that the net worth of households rose from

about 500% to more than 600% of disposable income in 1999 alone, and some people have argued that this rise completely outweighs any adverse effect from household debt,

which has been inching up to a mere 100% of income. However, this argument suffers from two flaws. First, apart from the fact that asset prices may well

fall substantially, the decisive constraint on borrowing may come not from the extent to which net worth is being mortgaged, but from the extent to which payments of

interest and repayments of principal (which must be settled in cash) can be met out of conventional income. It is income rather than net worth that is ultimately

the criterion of creditworthiness, since in a crisis it may be impossible for everyone to realise assets simultaneously. Second, the argument that

households' net worth has risen a lot does not touch the fact that half of the nonfinancial private debt is owed by businesses. Corporate debt has been rising

rapidly relative to corporate GDP for the last 2½ years and now exceeds levels last seen in the 1980s, when the last debt crisis unravelled.

If private net saving were to recover over the next few years to the level that is normal in other countries and that was normal in the United States until fairly

recently, the results would be horrendous. With private expenditure falling by 5 to 10% relative to income, there could be hardly any growth at all for some

years. If the unravelling took place as quickly as it did in the United Kingdom, there could be a severe recession, with grave consequences for the rest of

the world. The budget surplus would disappear. And it is easy to imagine that with a recession, or even a prolonged stagnation, there would be a large fall

in the stock market, which would make matters infinitely worse.

A Policy Reorientation to Change the Scenario

It would be possible for the authorities to reorient policy so as to avoid the whole scenario I have just outlined. Any fall in private spending could, at

least in theory, be offset by a relaxation of fiscal policy, which might have to take place even though the budget was already moving back into deficit. It is

difficult to see how the growing external deficit can be stemmed, as it eventually must, without there being, at some stage, a substantial fall in the dollar. It

is to be hoped that contingency planning along these lines is in hand, even though it runs slap contrary to conventional thinking at the moment.

While I believe continued prosperity in the United States to be at grave risk without a major change in fiscal and exchange rate policy at some stage, I would be a

fool to try to put a date on the turning point. I simply do not know when it will come.

Related Levy Institute Publications

L Randall Wray Can the Expansion Be Sustained? A Minskian View Policy Note 2000/5

Wynne Godley Interim Report: Notes on the US Trade and Balance of Payments Deficits Strategic Analysis Series 2000

Wynne Godley and Bill Martin How Negative Can US Saving Get? Policy Note 1999/1

Wynne Godley and L Randall Wray Can Goldilocks Survive? Policy Note 1999/4

L Randall Wray Surplus Mania Policy Note 1999/3

Source: © 2000 by The Jerome Levy Economics Institute: The Jerome Levy Economics Institute publishes research with the conviction that it is a constructive and positive

contribution to discussions and debates on relevant policy issues. Neither the Institute's Board of Governors nor its Board of Advisors necessarily

endorses any proposal made by the author.

Forget Handouts; Spur Production

To those who charge that liberalism has been tried and found wanting,

I answer that the failure is not in the idea, but in the course of recent history.

The New Deal was ended by World War II. The New Frontier was closed by Berlin and Cuba almost before it was opened.

And the Great Society lost its greatness in the jungles of Indochina.

- George McGovern

by Price Fishback and Shawn Kantor

With the hodge-podge of programs proposed to alleviate the current recession, it is worthwhile to look back

to the time in US history when the federal government first stepped in with massive stimulus programs: the New Deal.

President Roosevelt's 1930s programs consisted of five major categories:

| large-scale civil infrastructure such as the Hoover Dam, interstate road construction and water and sewer works |

| programs that provided direct relief for people and make-work or small-scale jobs such as building sidewalks or post offices |

| subsidies to farmers |

| loans to state and local governments, homeowners, bankers and industries |

| the insurance of mortgages and home improvement loans by the Federal Housing Administration. |

Inside the Roosevelt administration, there was a deep philosophical division. Public Works Administration head Harold Ickes fought for careful planning of large-scale

projects that would have lasting effects on the economy, even if it meant delays in the distribution of funds. Harry Hopkins, the

administrator of the major relief programs, argued for distributing money to the unemployed quickly, with fewer worries about the long-term value of the projects.

Our research suggests that Ickes' was the better approach. An additional dollar spent on building

large-scale infrastructure projects raised income by approximately $2. These projects not only provided

jobs for the unemployed but also raised the productivity of the private sector and of state and local governments.

The relief programs had much smaller effects on the economy. Certainly, the people getting direct help

benefited, but the nature of the projects appear not to have led to the kind of spillovers that stimulated

productivity in the private sector. Further, the huge infusion of federal funds allowed state and local governments to spend less.

Federal spending on New Deal agricultural programs, which paid farmers to remove land from production, had

the unintended consequence of diminishing consumer spending. The reduction in cultivation meant farms

needed less labour. The payments also encouraged farmers to mechanise and to use their available land more

productively, which further lowered the demand for labour. Thus, unemployment and lower incomes among farm labourers - and less spending.

The New Dealers also experimented with a wide range of loan programs, but these had little effect on the depressed economy. While the loans provided an immediate infusion

of cash, state and local governments raised taxes or collected reserves in anticipation of retiring the debt.

But the mortgage insurance program had a significant effect on the economy. The FHA insured loans for

home repairs and mortgages for both new and existing homes, which helped stimulate the construction

industry. For each additional dollar of mortgage and home improvement loans insured by the FHA in an area,

retail sales grew by about 90 cents. The program introduced a structural change in mortgage lending by

lengthening loan amortisations and altering terms of down payments. Monthly payments dropped, leaving homeowners with more money to spend.

What lessons can be learned from the New Deal?

Simply showering money on the economy is not enough. The spending programs that stimulated the economy

most during the 1930s succeeded because they raised the productivity of the economy generally, not simply benefiting those directly employed on the projects.

As the president and Congress debate an economic stimulus package, they should not expect dramatic results

unless they take care to cull the wheat of long-term productivity effects from the chaff of simple handouts.

Price Fishback and Shawn Kantor are professors of economics at the University of Arizona.

Source: Los Angeles Times Friday 30 November 2001

For more articles relating to Money, Politics and Law including globalisation, tax avoidance, consumerism, credit cards, spending, contracts, trust, stocks, fraud, eugenics and

more click the "Up" button below to take you to the Table of Contents for this section.

|  Animals

Animals Animation

Animation Art of Playing Cards

Art of Playing Cards Drugs

Drugs Education

Education Environment

Environment Flying

Flying History

History Humour

Humour Immigration

Immigration Info/Tech

Info/Tech Intellectual/Entertaining

Intellectual/Entertaining Lifestyles

Lifestyles Men

Men Money/Politics/Law

Money/Politics/Law New Jersey

New Jersey Odds and Oddities

Odds and Oddities Older & Under

Older & Under Photography

Photography Prisons

Prisons Relationships

Relationships Science

Science Social/Cultural

Social/Cultural Terrorism

Terrorism Wellington

Wellington Working

Working Zero Return Investment

Zero Return Investment