Animals

Animals Animation

Animation Art of Playing Cards

Art of Playing Cards Drugs

Drugs Education

Education Environment

Environment Flying

Flying History

History Humour

Humour Immigration

Immigration Info/Tech

Info/Tech Intellectual/Entertaining

Intellectual/Entertaining Lifestyles

Lifestyles Men

Men Money/Politics/Law

Money/Politics/Law New Jersey

New Jersey Odds and Oddities

Odds and Oddities Older & Under

Older & Under Photography

Photography Prisons

Prisons Relationships

Relationships Science

Science Social/Cultural

Social/Cultural Terrorism

Terrorism Wellington

Wellington Working

Working Zero Return Investment

Zero Return InvestmentExpandable/Expendable

It Keeps on Growing and GrowingIn our egalitarian democracy we have just about empowered a branch of the government, the FHA, to specify the size and shape of the typical American suburban master bedroom in which all Americans are thus created equal. - Peter Blake Freddie Mac UpdateBehind The Bloodbathby Daniel Kadlec and Adam Zagorin What does it mean when a company under criminal investigation sweeps out three top executives but only one is fired? That happened last week at Freddie Mac, the giant government-chartered mortgage company whose board grew impatient with management's internal probe of accounting irregularities that surfaced in January. Freddie Mac's president, David Glenn, was terminated, but the former chief financial officer, Vaughn Clarke, merely resigned and the former CEO, Leland Brendsel, retired at 61. The varying nature of their departures has grabbed the attention of Republican Congressman Richard Baker, who chairs a House financial-services subcommittee. Sources tell Time magazine that Baker has demanded documents in searching for clues that the two execs not fired were given an easy out. (Brendsel stands to collect $24.3 million severance; Clarke's package was not disclosed.) Glenn is the only executive specifically implicated so far. Freddie Mac says Glenn refused to cooperate with the internal probe and at one point ripped pages out of a diary. The Justice Department and the Securities and Exchange Commission are also investigating the company's finances. The stakes couldn't be higher. Freddie Mac holds or insures mortgages totaling $1.3 trillion. Any lasting scandal could drive up its borrowing costs and lead to higher mortgage rates - slowing a housing market that for three years has been the economy's main driver. Source: time.com from the Monday 23 June 2003 issue of TIME magazine

Mortgage-Lending Agencies in America: Big Scary Monsters

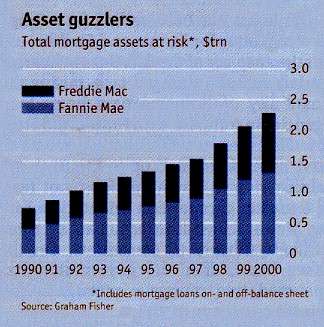

The driving force behind what little economic growth is now taking place in the world is, you might argue, America's housing market. The main impact of the Federal Reserve's six interest-rate cuts so far this year has been to trigger a slew of mortgage refinancings and other borrowing against the value of homes. This, in turn, has put extra cash in the hands of consumers, enabling them to spend more than might otherwise have been expected in the face of a sharp economic slowdown. It has also kept house prices strong - outside San Francisco and New York, two cities that are peculiarly sensitive to the stockmarket's fortunes-creating a benign "wealth effect" on consumer spending. That has taken much of the sting out of the malign effect of falling share prices. The main transmission mechanism between Fed rate cuts and the home owner are some mortgage-lending agencies with significant, though opaque, government backing: Fannie Mae (the Federal National Mortgage Association) and Freddie Mac (the Federal Home Loan Mortgage Corporation). These buy and issue mortgages, which they then securitise by bundling together by the thousand and selling in the debt markets. Between them, Fannie Mae and Freddie Mac either own, or insure the risk on, 40 - 45% of America's residential mortgages. Combined, their mortgage assets are now two-thirds as big as America's publicly traded government debt. Some analysts think they are on course to exceed public borrowing by the government by 2005. Indeed, given the strong and growing investor belief that the government will never allow Freddie or Fannie to fail, there is a case for viewing their borrowings as de facto government debt. The agencies run a formidable lobbying operation in Washington, yet their financial clout is coming under political scrutiny. In the past few weeks, George Bush's administration has taken a tougher stance towards them, albeit one whose effects will not be felt so swiftly that America's economic problems are made worse. On July 17th the administration backed new, more prudent rules for risk-based capital adequacy, due to bite in a year. It also talks privately about measures to put competitive pressure on Fannie Mae and Freddie Mac, by licensing new rivals. The spectacular growth of Fannie and Freddie is troubling in several ways, both practical and theoretical. Their activities certainly help to keep the economy above water. Yet, says John Lonski, an economist at Moody's, a credit-rating agency, the economy relies too much on a single sector, housing, to avoid recession. Much of the increase in housing debt has happened because people have borrowed against the equity in their homes, ie, against the value of the properties minus existing mortgages. This way, owners are more exposed to a fall in house prices. And house' prices might well fall, should the economy move decisively into recession, which is still a risk. Mortgage debt in America is now $5.1 trillion, up from $3.4 trillion in 1995. Giant mortgage lenders, in effect guaranteed by government, distort the economy's allocation of capital, argues Bert Ely, a Washington-based economist. Indeed, there may right now be the makings of a bubble in house prices.

Answers to these questions take several forms. Perhaps housing loans should be subsidised, particularly for the poor, because home ownership is desirable. Even if true, this only partly gets Fannie and Freddie off the hook. For their ambitions focus ever more on moving upmarket. They are lobbying for the cap on mortgages that they can offer to rise, from $275,000 to $412,000 - to help the "ill-housed wealthy", perhaps, murmurs one analyst? A recent study by the Congressional Budget Office provoked the agencies' fury by claiming that the advantages they enjoyed were far larger than had been thought, and that much of the benefit of the government subsidy went to shareholders rather than borrowers. For their part, Fannie Mae and Freddie Mac argue that they are not really backed by the government, so they enjoy minimal competitive advantages. This claim is absurd. It also sits uneasily with their strategy of turning their debt into the main benchmark for fixed-income securities, replacing treasury bonds, and with plans to sell their debt to retail investors as a low-risk investment. There are big questions, too, about the quality of their lending and risk management. Congressman Richard Baker, a tireless critic of the two agencies, has wondered if they might not become the source of the next global financial crisis. Credit losses have been increasing, and the agencies' leverage is scary. According to calculations by a research firm, Graham Fisher, their debt-to-equity ratio ranges from 30 to as much as 84, depending on what assumptions are made about off-balance-sheet exposures. Further, new accounting standards that require fuller disclosure of derivatives losses raise fresh questions about the adequacy of the agencies' capital, never as large relative to loans as at the big retail banks. Declining capital adequacy may yet force the agencies to cut back their activities. Mr Baker has been calling for a tough new regulator for Fannie and Freddie, under the auspices of the Fed. But at a hearing on July 11th, he changed tack, raising the possibility of licensing new home-loan agencies to compete with Fannie and Freddie. This idea, worth debating, seems to have come from high up in the Bush administration. It has attractions, not least that greater competition might force Fannie Mae and Freddie Mac to pass on more of their subsidy to consumers. On the other hand, after the government has spawned two mortgage monsters, is it wise to create anymore? Source: The Economist 21 July 2001

The "sting" of falling share prices was removed because people borrowed against their homes to get spending money? Why, what a good idea! Americans are so clever.

For more articles relating to Money, Politics and Law including globalisation, tax avoidance, consumerism, credit cards, spending, contracts, trust, stocks, fraud, eugenics and

more click the "Up" button below to take you to the Table of Contents for this section. |

For the government to underwrite a huge piece of the credit-creation industry also raises broader

questions. Why do it at all? And, if housing, why hot business lending? Both Fannie and

Freddie are publicly traded companies, and their shareholders, which have included Berkshire Hathaway, run

by Warren Buffett, have benefited handsomely from their implicit government guarantees.

For the government to underwrite a huge piece of the credit-creation industry also raises broader

questions. Why do it at all? And, if housing, why hot business lending? Both Fannie and

Freddie are publicly traded companies, and their shareholders, which have included Berkshire Hathaway, run

by Warren Buffett, have benefited handsomely from their implicit government guarantees.