Animals

Animals Animation

Animation Art of Playing Cards

Art of Playing Cards Drugs

Drugs Education

Education Environment

Environment Flying

Flying History

History Humour

Humour Immigration

Immigration Info/Tech

Info/Tech Intellectual/Entertaining

Intellectual/Entertaining Lifestyles

Lifestyles Men

Men Money/Politics/Law

Money/Politics/Law New Jersey

New Jersey Odds and Oddities

Odds and Oddities Older & Under

Older & Under Photography

Photography Prisons

Prisons Relationships

Relationships Science

Science Social/Cultural

Social/Cultural Terrorism

Terrorism Wellington

Wellington Working

Working Zero Return Investment

Zero Return InvestmentBad News Offered Up on a Cushion

Inherent Uncertainty Regarding Continuation of a Going ConcernHe who laughs has not yet heard the bad news. - Bertolt Brecht Without qualification to the opinion expressed above, attention is drawn to the following matter. As a result of the matters described under the basis of accounting note, there is significant uncertainty as to whether the company and the economic entity will be able to continue as a going concern and therefore whether the company and the economic entity will be able to realise their assets and extinguish their liabilities in the normal course of business and at the amounts stated in the financial statements and whether the company and the economic entity will be able to pay their debts as and when they fall due. The financial statements do not include any adjustments to the recorded amounts of assets and liabilities that may be necessary should the company and the economic entity not be able to continue as a going concern. Source: an Annual Report from a foreign company which I found lying on a ledge at the post office in Marion Square, Wellington

I guess the reason this attracted my attention is that I sympathised with the recipient - an investor hearing some very bad (and possibly unexpected) news. I wonder if those shareholders got to attend a shareholder meeting so they they could ask any last questions they might have about what went wrong. (We certainly didn't - see Trust Topples, The Final Word on Having a Meeting.)

All Time Record Set for Bankruptcies in the Year ended 31 March 2003

Bankruptcy cases broke a record for the year ended 31 March 2003. The number of filings exceed 1.6 million for the first time in any 12 month period. The number of bankruptcy petitions filed in federal courts rose 7.1% in the 12-month period, according to statistics released by the Administrative Office of the US Courts. Bankruptcy filings rose from 1,504,806 in the 12-month period ending March 2002 to 1,611,268 in the same 12-month time period in 2003. The number of filings continues to break records. The previous highest total of filings for any 12-month period was in the 12-month period ending 31 December 2002, with a total of 1,577,651. Business filings in March 2003 totaled 37,548, down 5.8% from the 39,845 business filings in the 12-month period ending March 31, 2002. Non-business filings totaled 1,573,720, up 7.4% from the total non-business filings of 1,464,961 in the 12-month period ending 31 March 2002. This also is a record number of non-business filings for any 12-month period. Statistics are from the Administrative Office of the Courts

Bankruptcy Profiles

Sourced from The Fragile Middle Class: Americans in Debt by Elizabeth Warren, Harvard Law School and from Smith Business Solutions The typical family filing for bankruptcy in 1997 owed more than 1½ times its annual income in short-term, high-interest debt. For example, a family earning $50,000 had an average of $75,000 in credit card and similar debt. Source: bankruptcyaction.com 15 May 2003

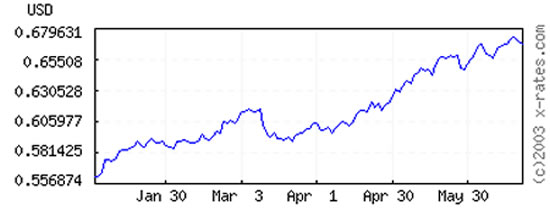

US Dealer Blamed for Aussie's Fall

120 Day Graph The following article was actually written almost three years ago. However, as the graph illustrates, not too much has changed... by Jack Taylor A US currency trader was accused of playing a key role in the slump of the Australian dollar, which hit an all time low last week amid desperate government efforts to prop it up. As analysts search for an explanation for Australia's simultaneously having one of the world's strongest economies and one of the weakest currencies, Sydney's Sun-Herald named US speculator Richard Dennis as the principle cause of the slump of the "Aussie." Chicago-based Dennis is said to have sold A$400 million (US$208 million) on 28 January, sparking an avalanche against the Aussie from which it has never recovered - "because he saw an opportunity to make a quick buck." The selling has continued ever since and the dollar, which reached a six-month high of US66.64¢ in January, had dropped 22.5% to an all-time low US51.65¢ last week before clawing its way back above US52¢. Australian Treasurer Peter Costello has spent the last few days in New York trying to prop up the local currency. He spoke to major Wall Street traders and influential investors to try to persuade them to reassess it in the light of Australia's sound economic fundamentals, such as a strong budget surplus, low inflation and rising productivity. He will also attend the meeting in Montreal of the G20 group of nations to discuss, among other issues, international currency instability and options for dealing with it. The meeting will also discuss the persistent weakness of the euro, which has also been targeted by currency traders in recent weeks. Dennis was described as a big-time speculator who turned US$400 into a personal fortune of more than $200 million in the last 18 years, using what he called "the turtle system" - identifying a trend and sticking to it. His assault on the Aussie began when he saw data showing Australia's lower than expected inflation rate as a signal that the country would not raise interest rates as they were expected to do in the United States. His decision to dump the Aussie saw it plunge that day by more than 5%, a fall of US 3¢ to US62.25¢ - its biggest one day drop in three years. Dennis could not be reached for comment, but his colleague Wesley Covel told the Sun-Herald: "The Aussie has become a great currency to short and make money as it sinks downward. Lots of money is being made as it goes down." Selling short means betting how low the currency will go over the next few hours. When traders all over the world do this it drives the currency down, regardless of what its true levels should be. If true - and many observers here have suspected it for months - it makes a mockery of comments by supposed experts about the likely causes of the depreciation. Some analysts have linked it to Australia's persistently high current account deficit or to the fact that Australia is perceived as having an old economy dependent on primary exports and inadequate high-tech industry. But, according to the Sun-Herald, speculators like Richard Dennis and Wesley Covel know or care little about the shape of the Australian economy. "Who cares if the economy is sound?" said Covel. "The trend is down, so traders short the currency. It's as simple as that." Source: Bangkok Post Business International page Monday 23 October 2000

Can cause and effect be completely separated here? Is everyone just looking for someone else to blame?

Richard Dennis

Richard Dennis had an office tucked away on the antiquated 23rd floor of the Chicago Board of Trade building. The outside hallway had dingy brown panelling. Etched in small lettering in his office door was "C&D Commodities, Richard J Dennis and Company." No marble. No glass. Immediately next door was a grimy looking men’s room. The office entrance disguised the performance of an individual who, in his own estimate, made between $100 million and $200 million. Q. How did you first get involved in commodity trading? Dennis and the Turtles: As a trader and teacher, Dennis is without peer. How did the Turtle selection process work? During the selection process Mr Dennis asked applicants to describe the riskiest thing they had ever done. He wanted to see if they took calculated risks or risk for its own sake. The answers he got ranged from one applicant who drove an hour to a basketball game without having a ticket to get in, to another applicant who drove around Saudi Arabia for several months with whiskey in his car trunk, a serious offense. The first applicant was admitted to the program. The second applicant wasn't. QuotesI don't think trading strategies are as vulnerable to not working if people know about them, - Richard Dennis Unlike Eckhardt (and most other savants) Dennis believed that trading could be taught and learned. - Barclays Report ...he placed classified ads proclaiming "trader wanted," and got some 1,000 responses - Business Week Richard Dennis should be saluted for his skills as a trader and teacher. His instruction given to the Turtles was one of the great financial stories of all time. The Turtles' success as Trend Followers is unquestioned. Trend Following philosophy has stood the test of time. Trend Following Turtles will mint money as long as there are markets to be traded. Dennis himself has made hundreds of millions of dollars over the years. But while his students have had successful money management careers, Dennis seems to not mesh well with clients. If Dennis just traded for himself he would be fine (and much richer). His problems begin when he trades for impatient clients. His most recent stab at managing money (which ended in fall 2000) for others resulted in a compound annual return of 26.9% (after fees), including two years when performance exceeded 100%. But, he recently stopped trading due to client impatience plain and simple. His clients pulled their money right before his trading would have gone straight up. Doubt us? Use Dunn Capital as a proxy and you will see what happened in the fall of 2000. One of the biggest lessons traders should learn is that trading for your own account and trading for customers are two different things. John W Henry has said on many occasions that it never gets easy losing money for clients. Traders that just concentrate on expanding their own capital often have a great advantage over money managers. Money managers always deal with the pressure and expectations of customers (rightly or wrongly). Source: turtletrader.com

Riding Herd on the MarketFundamentals Versus Trends by Kenneth Chang Computers can be irrationally exuberant, too. Ever wonder what causes financial markets to jump up and down for no apparent reason? Well, traders sometimes just chase the crowd in search of a profit, a computer simulation shows. "We have defined a market with a multitude of traders who use different types of strategies," says Thomas Lux, an economist at the University of Bonn in Germany. "It brings out an element of herd behaviour into the market." Most economic theories assume that traders act "rationally," that the price of a company or commodity reflects its fundamental worth based on earnings, debt and future prospects. However, this thinking can't explain, for example, the skyrocketing values of Internet companies that have never turned a profit. Lux, along with Michele Marchesi of University of Caliari in Italy, constructed a computer model in which 500 virtual traders traded one commodity, similar to how a foreign exchange market works. Some of the traders used a strategy that hinged upon the commodity's fundamental value, which fluctuated randomly. Others traded based on market trends, a sort of "trader see, trader do" strategy. Virtual traders could also switch strategies depending on which seemed to be doing better. The result: the market price varied more wildly than the underlying value. The patterns and statistics of the price swings also more closely matched those of real-world markets than those predicted by strictly rational trading behaviour. "We see in our model, the price dynamics reflect fundamental values but only to an extent," Lux says. "We think this shows one needs to pay more attention, one has to stress more the interaction of agents, which has been neglected in economics up to now." Lux and Marchesi reported their results in last week's issue of the journal Nature. Lux and Marchesi are "probably the first" to take this approach to studying markets, comments Masanao Aoki, professor emeritus of economics at the University of California, Los Angeles. The researchers, he says, are "basically saying the volatility of the market is due to the mixture of the two types of traders." According to Lux, when the market is calm and everyone is trading based on just the fundamental value, no one earns much. "All the strategies in the model have the same pay-off," Lux says, "namely a pay-off of zero." That leads the computer-model traders to try the other technique, looking to take advantage of market trends. "They play around," Lux says. "This may lead to the formation of price bubbles." Once some start making money, others join the market-trend approach until the bubble breaks. "Then we have volatility, and everybody is [again] a fundamentalist," Lux says. "That's a typical outcome of our model and that's close to what traders usually report. In certain periods, it pays more to forget about the fundamentals. In other periods, it pays more to follow the fundamentals." The results come as no surprise to those working in the markets. Traders "tend to be eclectic in their approach to making their decisions," says Joseph Liro, vice president of Stone and McCarthy Research Associates in Princeton, NJ. "It very much depends on market conditions." Lux's model also offers discouraging prospects for beating the market. In one variation of the simulation, one market-trend trader used a sophisticated neural network approach for deciding when to buy and sell, while all the market-trend traders used a simple algorithm. The sophisticated trader did no better than its peers. "On average, our traders do not outperform the others," Lux says. "It is a zero-sum game on our market." On a larger scale, the study might give policy makers food for thought about how financial markets are run and regulated. "Our models show the ways in which this market risk is created," Lux says, "and then you can think about policy decisions to decrease the risk." Source: ABC15 Feb 2000

For more articles relating to Money, Politics and Law including globalisation, tax avoidance, consumerism, credit cards, spending, contracts, trust, stocks, fraud, eugenics and

more click the "Up" button below to take you to the Table of Contents for this section. |